The current default form of investment as securities trading has a monopoly on our thinking about enterprise, investment, society, the economy and the environment.

Is such a monopoly a good thing?

Partnering Stewardship Investors with Values-Driven Business Leaders to Build a Future of Sustainable Prosperity

Sunday, September 29, 2013

Saturday, September 28, 2013

Copernican Revolutions to Restore Equality of Economic Opportunity and a Functioning Democracy

In Robert Reich's documentary, Inequality for All, they make the point that the consumer is the center of the economy. like the sun at the center of the solar system.

Evergreen is a form of investment built on a customer/cash flow centered model of the enterprise. See below.

This is one of two Copernican revolutions in evergreen investing. This on replaces production that is the center of enterprise in the current default form of investing as securities trading with customer cash flows.

The other replaces Wall Street at the center of a trading universe with stewardship investors at the center of a direct investing universe.

Evergreen is a form of investment built on a customer/cash flow centered model of the enterprise. See below.

This is one of two Copernican revolutions in evergreen investing. This on replaces production that is the center of enterprise in the current default form of investing as securities trading with customer cash flows.

The other replaces Wall Street at the center of a trading universe with stewardship investors at the center of a direct investing universe.

Friday, September 27, 2013

Connecting the Dots on Inequality

Last night I attended the Boston area premiere of Robert Reich's new documentary, "Inequality for All", at the Kendall Square Cinema in Cambridge.

The movie tells many powerful stories about the growing wealth inequality in this country.

Here is one story it does not tell. Can you imagine it as an animation in your mind's eye?

The movie tells many powerful stories about the growing wealth inequality in this country.

Here is one story it does not tell. Can you imagine it as an animation in your mind's eye?

- It starts with you, and each of us, as individuals working hard to build something we each treasure, and collectively we all treasure: savings held for investment and reinvestment, so that we may live well in our retirement, and have something to pass on to the next generation,

- We give those savings to pensions as stewards of our future, to invest and reinvest, prudently, on our behalf - imagine this as a physical transfer

- Pensions give our savings to experts in the default form of investment as securities trading, who take us on the bumpy ride, buying low and selling high.

- Fiduciary duty should shout: STOP!. Speculating is not allowed, because it is too dangerous.

- Economics pushes fiduciary duty out of the way, giving us all its assurances that speculation can be made safe through diversification and disclosure.

- We get: 2008. The markets collapse, the global economy comes to a virtual standstill.

- The Advisor (dressed as a wizard, in flowing robes and a pointy hat: a Wizard of Wall Street) comes in, saying in a very pleased tone "delighted to report that your volatility was well controlled and your fund outperformed the benchmark and median".

- The pension fiduciary turns round to the Wizard in shock and dismay, and says "what the xxxx does that mean?".

- The Wizard says "you lost money but not as much as other folks and its meaningless 'cause they are talking about 3 years".

- Evergreen steps forward and pushes the Wizard away, saying diversification and disclosure only work for the little guy, that needs liquidity. For large, purposeful, powerful stewards of an evergreen trust, that needs longevity more than liquidity, they are not enough.

- Evergreen says, "Evergreen stewards have the power to 'go long' themselves, directly, and take back control of the decision to reinvest."

- Fiduciary duty steps back in and says: "Pensions must go Evergreen, because they can. If they can, then they should. Anything else is not prudent, and is not loyal."

- Speculation fades away. It has nothing to say.

- Business Strategy says, "You're right"

- Casino Capitalism becomes once again Creative Capitalism, but this version is new and improved. Creative Capitalism 2.0: robust, resilient, regenerative and adaptively co-creative. A kinder, gentler Creative Capitalism. For society. The economy. The environment. People and Planet, alongside Profit!

Wednesday, September 25, 2013

Capital Institute on Evergreen Investing

Capital Institute has published a Field Guide Study on evergreen investing as co-creating a regenerative economy.

You can find it in the spotlight at www.capitalinstitute.org

You can find it in the spotlight at www.capitalinstitute.org

Tuesday, September 24, 2013

Evergreen is for Everybody

It takes size to negotiate investment directly with enterprise. It takes purpose. It takes longevity. It takes leverage.

As individuals, we do not have the size, the purpose, the longevity or the leverage it takes to negotiate. We are small, idiosyncratic, time-limited, and therefor leverage limited. The default form of investment as securities trading is a good fit for our small scale, idiosyncratic and highly liquid investment needs and capabilities as individual investors investing for our own account.

As participants in a pension plan, however, we do, collectively, have the size, the purpose, the longevity and the power to negotiate. Or rather, our pension trustees do, when investing "other people's money" -- our money -- on our behalf and for our benefit. The new form of evergreen investment is a good fit for large, purposeful and powerful pension plans and other evergreen trusts investing for the collective benefit of successive generations of current and future retirees or other chartered beneficiaries.

The choice of evergreen investing by pensions and other evergreen trusts is important to those trusts, to their trust sponsors and to their sponsored beneficiaries. It is also important to all of us, because it affects the proper flow of money through the economy.

Evergreen investing by evergreen trusts flows money directly into enterprises that are also evergreen, to sponsor the ongoing work of physical wealth creation that is also evergreen. There is matching, alignment and balance. A healthy flow.

The default form of securities trading by evergreen trusts traps money inside the closed loop of a zero-sum game of extracting value from other investors, including other evergreen trusts. There is bloat, not balance.

This affects more than just the trusts. It affects us all.

As individuals, we do not have the size, the purpose, the longevity or the leverage it takes to negotiate. We are small, idiosyncratic, time-limited, and therefor leverage limited. The default form of investment as securities trading is a good fit for our small scale, idiosyncratic and highly liquid investment needs and capabilities as individual investors investing for our own account.

As participants in a pension plan, however, we do, collectively, have the size, the purpose, the longevity and the power to negotiate. Or rather, our pension trustees do, when investing "other people's money" -- our money -- on our behalf and for our benefit. The new form of evergreen investment is a good fit for large, purposeful and powerful pension plans and other evergreen trusts investing for the collective benefit of successive generations of current and future retirees or other chartered beneficiaries.

The choice of evergreen investing by pensions and other evergreen trusts is important to those trusts, to their trust sponsors and to their sponsored beneficiaries. It is also important to all of us, because it affects the proper flow of money through the economy.

Evergreen investing by evergreen trusts flows money directly into enterprises that are also evergreen, to sponsor the ongoing work of physical wealth creation that is also evergreen. There is matching, alignment and balance. A healthy flow.

The default form of securities trading by evergreen trusts traps money inside the closed loop of a zero-sum game of extracting value from other investors, including other evergreen trusts. There is bloat, not balance.

This affects more than just the trusts. It affects us all.

Monday, September 23, 2013

Competition for the Monopoly of Valuations as the Default Form of Large-Scale Investment

The current default form of investment as securities trading is built on formulas for calculating the value of an expected future stream of wealth-creating events that have not happened yet as a specific price at a specific time. It is actually based on two specific prices at two different times, one more specific than the other: the buy, and the sell.

Evergreen investing is different. Evergreen investing is built on sharing directly in wealth creation as it happens, over time. It works by agreement between enterprise and investment on formulas for sharing in enterprise cash flows, if, as and when they flow through the enterprise.

This is the form of investment that is the default choice for large-scale investors when investing in wealth creation of the real estate kind. Evergreen takes this form, and makes it available for investment in enterprise for wealth creation of any kind.

In the process, it is creating a new form of market for investment. One that offers a whole new choice.

It is a choice that will break the monopoly of the current default form.

Evergreen investing is different. Evergreen investing is built on sharing directly in wealth creation as it happens, over time. It works by agreement between enterprise and investment on formulas for sharing in enterprise cash flows, if, as and when they flow through the enterprise.

This is the form of investment that is the default choice for large-scale investors when investing in wealth creation of the real estate kind. Evergreen takes this form, and makes it available for investment in enterprise for wealth creation of any kind.

In the process, it is creating a new form of market for investment. One that offers a whole new choice.

It is a choice that will break the monopoly of the current default form.

Sunday, September 22, 2013

All Valuations Are Wrong

How do you measure something that has not happened yet?

You can't. Data is always historical. We can only measure what is.

The future, we can calculate, if it is repeating, or expect, if it is not.

Science and engineering calculate the future by studying the past. Scientists and engineers study data collected on past events to discover patterns that repeat at regular intervals under specified circumstances. When the circumstances change, they change their patterns. In some circumstances, their patterns become only expectations. They expect, but they do not really know. The patterns don't really repeat, at least not in ways that we can see. The world, or at least our knowledge of the world, is still evolving.

Such is the case with financial valuations within the current default form of investment as securities trading. The price at which securities trade is always only an expectation, a guess at what is not yet known, because it has not yet happened.

The theory posits that the market will always get the price right. Experience shows the market always gets the price more or less right. That "more or less" makes the difference between profit and loss in a trading position. Market professionals call it "risk".

Portfolio theory holds that price risk is random, and this randomness can be canceled out by the Law of Large numbers: repeat the same action enough times and random outcomes will settle down into a predictable pattern. Diversify across enough trading positions, and volatility will settle down into capital appreciation over time.

Experience shows that expectations are not wrong through random error. They are wrong because we cannot see that far into the future.

Things change, and we adapt. We learn new things. We shape new possibilities. We make new choices. We take new actions. We create our own future.

Our future is not repeating. It is evolving. Evolution cannot be calculated. It must be experienced.

The current default form of investment as securities trading is built on calculations of that which cannot be calculated. It's valuations are always only more or less right, which means they are always also more or less wrong. They are not really calculations based on repeating patterns. They are calculations based on expectations for what will happen, but has not happened yet.

For us, as individuals, our time is limited. At some point, our clock runs out, and the expectations stop. Relative to investment, we only care about the future for so long.

But what about an evergreen trust? The clock for a pension plan never runs out. It just keeps going. So, the expectations never stop.

This is not easy to see at first, but it merits attention. Think about it.

You can't. Data is always historical. We can only measure what is.

The future, we can calculate, if it is repeating, or expect, if it is not.

Science and engineering calculate the future by studying the past. Scientists and engineers study data collected on past events to discover patterns that repeat at regular intervals under specified circumstances. When the circumstances change, they change their patterns. In some circumstances, their patterns become only expectations. They expect, but they do not really know. The patterns don't really repeat, at least not in ways that we can see. The world, or at least our knowledge of the world, is still evolving.

Such is the case with financial valuations within the current default form of investment as securities trading. The price at which securities trade is always only an expectation, a guess at what is not yet known, because it has not yet happened.

The theory posits that the market will always get the price right. Experience shows the market always gets the price more or less right. That "more or less" makes the difference between profit and loss in a trading position. Market professionals call it "risk".

Portfolio theory holds that price risk is random, and this randomness can be canceled out by the Law of Large numbers: repeat the same action enough times and random outcomes will settle down into a predictable pattern. Diversify across enough trading positions, and volatility will settle down into capital appreciation over time.

Experience shows that expectations are not wrong through random error. They are wrong because we cannot see that far into the future.

Things change, and we adapt. We learn new things. We shape new possibilities. We make new choices. We take new actions. We create our own future.

Our future is not repeating. It is evolving. Evolution cannot be calculated. It must be experienced.

The current default form of investment as securities trading is built on calculations of that which cannot be calculated. It's valuations are always only more or less right, which means they are always also more or less wrong. They are not really calculations based on repeating patterns. They are calculations based on expectations for what will happen, but has not happened yet.

For us, as individuals, our time is limited. At some point, our clock runs out, and the expectations stop. Relative to investment, we only care about the future for so long.

But what about an evergreen trust? The clock for a pension plan never runs out. It just keeps going. So, the expectations never stop.

This is not easy to see at first, but it merits attention. Think about it.

Friday, September 20, 2013

Evergreen Engineered Performance

Evergreen direct investing is purpose-built to empower large, purposeful and powerful stewards of an evergreen trust to:

- engineer investment performance;

- simplify investment design;

- internalize investment management;

- save on investment expenses; and

- exercise control over investment impacts on society, the economy and the environment.

The idea map, below, is offered to illustrate these features.

- Priority cash sweeps de-risk the investment by recovering entrusted funds and realizing a fiduciary level of return within the limits of an engineered base case. This happens during the earlier years, when the risks are more clear and strategies can be pre-agreed.

- Ongoing participation in ongoing cash flows by the investor beyond the base case makes the investment evergreen. This is "upside" to the investor.

- Increasing cash to enterprise leadership as pre-agreed performance milestones are passed rewards effective leadership and allocates risk of changes in the ecosystem of competition over time to those best able to adapt to those changes as things evolve.

- Interests of enterprise and investment are aligned around optimizing commercial competitiveness to sustainably generate open-ended, ongoing and evergreen cash flows.

Sunday, September 15, 2013

The New Wall Street Panopticon

Today's post is a short essay describing the Copernican Revolution that is redefining the panopticon of Creative Capitalism.

A panopticon is a building designed on a hub-and-spoke parti, or architectural pattern.

It is useful for giving clear lines of sight into all the activities taking place within a given built environment from a central hub. It is popular these days for libraries, where stacks radiate out from a central circulation hub.

Wall Street can be spatialized as a panopticon, with different classes of investors radiating out from Wall Street at the center. The purpose of this panopticon is to aggregate large pools of constant capital for investment in enterprise from a diverse and constantly changing population of actual funding sources. Its uniqueness is liquidity. A market operates within this panopticon that gives every participant the ability to sell out of any position, at any time. It does this by letting the sell price float to whatever level it must in order to effect a sale. This is the market-clearing price. It provides a certain sale, but at an uncertain price. It does this by connecting investors to other investors, anonymously and asynchronously, through Wall Street, which sits at the hub, finding the matches within the ever-changing population of speculators speculating on valuations in a valuations marketplace.

Pensions were for a long time only minor contributors of funds for trading in these markets. Traditional interpretations of fiduciary prudence limited these stewards of an open-ended, ongoing, regenerative, and therefor evergreen, trust to buying and holding dividend-paying stocks, as bond alternatives.

That changed in 1972. It changed because in 1969 the US tax laws were changed to require private foundations to pay out amounts equal to at least 5% of their entrusted corpus each year, in order to maintain their status as tax-exempt. Under then-prevailing interest rate conditions, returns on a portfolio of bonds and dividend stocks did not return 5%. That meant that foundations like Ford Foundation would have to choose between paying out corpus - which meant liquidating their trust over time, and putting themselves out of a job - or surrendering their tax-exempt status.

Instead, they invented a third alternative. Lead by the Ford Foundation, the stewardship community drove adoption of a new interpretation of the standards for fiduciary prudence. This new interpretation of fiduciary prudence let them pursue total return through capital appreciation by relying on diversification to protect against market volatility, as endorsed by Modern Portfolio Theory.

This change was made in 1972, with the widespread enactment of the Uniform Management of Institutional Funds Act. Since 1972, pensions have been full-on participants in the Wall Street panopticon for speculating on valuations in the valuations markets, buying and selling stocks in pursuit of capital appreciation that can only be realized by active trading.

Pensions are defined benefit ("DB") plans. Actuarial risk pools, actually, that rely on the Law of Large Numbers to socialize the costs of living in retirement across a statistically significant population of current and future retirees. The inverse of life insurance. Contributions vary as actuarial calculations say are necessary to provide income security in retirement to plan participants.

Pensions have always been popular with workers, and society more generally, but problematic for plan sponsors and administrators. Since the total amount of benefits to be paid are not ever really knowable (the plans being open-ended, ongoing, regenerative and therefor evergreen), it can never be certain that contributions will be adequate. This uncertainty gets magnified many times if actuarial assumptions about investment earnings are not realized in the event.

In 1978, an alternative approach to retirement savings was written into the US tax laws, in the form of various tax-deferred savings accounts. These are known as defined contribution ("DC") plans. The amounts contributed determine the amounts available to provide income during retirement. That, together with investment gains (or losses). DC plans put the risk and responsibility for investment management on each individual saver. Income security in retirement is not really assured, as the income runs out when the savings runs out, not when retirement ends.

These DC accounts are allowed to invest savings as the saver may decide. This innovation transformed the previously sleepy mutual fund business into a major market participant.

The growth in professionally managed retirement plans, both DB and DC, since the 1970s has been explosive. Not just in the US. Worldwide. According to research by Towers, Watson, globally, professionally managed DB and DC plans, combined, doubled over the 10 years from 2002 to 2012, from $15 Trillion to $30 Trillion USD. This represents something like half of the total estimated $60 Trillion USD available as capital for investment, worldwide.

This explosive growth in professionally managed retirement plans has transformed the dynamics of the Wall Street Panopticon. There is room for debate over whether that transformation is for the better.

The diagram below shows the current state of the Wall Street Panopticon, with most of the money available for trading controlled by Mutual Funds and Pension Funds, and with a proliferation of advisors attaching themselves to the lines that connect Pension Funds especially, but Mutual Funds as well, out on the periphery with the Wall Street market-clearing mechanisms at the hub.

Whatever one may think of the larger impact of this redistribution of control over savings held for investment, its impact on pension funds, in particular, has been adverse. Pensions are experiencing erratic returns, inadequate returns, misalignment of incentives, miscreant market manipulation, the orphaning of social, economic and environmental impacts and a growth in the zero-sum game of extracting value from other market participants, which means increasingly that each retirement plan is seeking to provide for its retirees at the expense of other retirement plans, and other retirees, who are participating in those other plans.

The "everybody wins" of wealth creating capitalism in its original incarnation has degenerated into the zero-sum game of Casino Capitalism that we are living with today. In consequence, there are those who contend that proper pension plans, DB plans that provide real, sustainable income security in retirement, cannot continue.

As the global financial crisis of 2008 demonstrated most recently and most dramatically, we all suffer adversely from this, as closed-loop trading of retirement savings drives overvaluations in the valuations markets that are unsustainable, creating an illusory prosperity that evaporates when the valuations collapse. We are getting too-big-to-fail that fails nonetheless.

The solution is not to be found by tweaking the current Wall Street Panopticon.

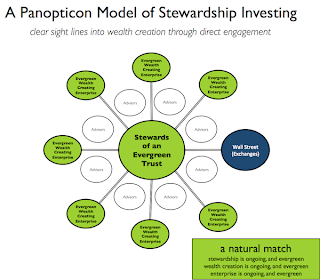

The solution is Copernican. We have to build a new stewardship panopticon that puts professional management of retirement savings at the center of its own investment universe, building for these stewards of open-ended, ongoing, regenerative - and therefor evergreen - trusts clear sight lines into equally open-ended, ongoing, regenerative and therefor evergreen wealth creation through direct engagement with wealth creating enterprises that are also open-ended, ongoing, regenerative, and therefor evergreen.

This is a natural match of evergreen to evergreen through direct participation in wealth creation over time that will empower pensions, in particular, to engineer portfolio returns to match their fiduciary responsibilities and reduce their exposure to systemic overvaluations in the valuations markets, while also simplifying portfolio design, internalizing portfolio management (to the extent they choose), reducing portfolio costs and increasing their control over portfolio impacts on society, the economy and the environment. It will empower defined benefit plans to continue providing real income security in retirement to successive generations of current and future retirees.

In this new evergreen stewardship panopticon, Wall Street is moved from the center to the periphery, where it continues to compete, as one enterprise among others, for funding from the stewards of our retirement security.

This is what makes it Copernican. The earth is no longer the center of the heavens, in which the sun is one object among many. Instead, we have a solar system, with the sun at the center, and the earth, as one planet among many, orbiting around the sun.

In this post-Copernican world, Wall Street will continue as the hub of its own panopticon for speculating on valuations in the valuations markets, with retirement stewards still forming one of many classes of market participants out on the periphery, but the volume of retirement savings being used to fund speculation on valuations within the New Wall Street Panopticon will shrink.

In the process, we will see Casino Capitalism shrink back down to a more authentic form of Creative Capitalism, but the new Creative Capitalism will be turbo-charged by access to two competing market systems: the familiar Wall Street panopticon for speculating on valuations in the valuations markets, and the new Stewardship Panopticon for direct engagement of evergreen trusts with evergreen enterprise for evergreen sharing in evergreen wealth creation.

The Current Wall Street Panopticon.

A panopticon is a building designed on a hub-and-spoke parti, or architectural pattern.

It is useful for giving clear lines of sight into all the activities taking place within a given built environment from a central hub. It is popular these days for libraries, where stacks radiate out from a central circulation hub.

Wall Street can be spatialized as a panopticon, with different classes of investors radiating out from Wall Street at the center. The purpose of this panopticon is to aggregate large pools of constant capital for investment in enterprise from a diverse and constantly changing population of actual funding sources. Its uniqueness is liquidity. A market operates within this panopticon that gives every participant the ability to sell out of any position, at any time. It does this by letting the sell price float to whatever level it must in order to effect a sale. This is the market-clearing price. It provides a certain sale, but at an uncertain price. It does this by connecting investors to other investors, anonymously and asynchronously, through Wall Street, which sits at the hub, finding the matches within the ever-changing population of speculators speculating on valuations in a valuations marketplace.

Pensions in the Current Wall Street Panopticon

Pensions were for a long time only minor contributors of funds for trading in these markets. Traditional interpretations of fiduciary prudence limited these stewards of an open-ended, ongoing, regenerative, and therefor evergreen, trust to buying and holding dividend-paying stocks, as bond alternatives.

A New Interpretation of Fiduciary Prudence.

That changed in 1972. It changed because in 1969 the US tax laws were changed to require private foundations to pay out amounts equal to at least 5% of their entrusted corpus each year, in order to maintain their status as tax-exempt. Under then-prevailing interest rate conditions, returns on a portfolio of bonds and dividend stocks did not return 5%. That meant that foundations like Ford Foundation would have to choose between paying out corpus - which meant liquidating their trust over time, and putting themselves out of a job - or surrendering their tax-exempt status.

Instead, they invented a third alternative. Lead by the Ford Foundation, the stewardship community drove adoption of a new interpretation of the standards for fiduciary prudence. This new interpretation of fiduciary prudence let them pursue total return through capital appreciation by relying on diversification to protect against market volatility, as endorsed by Modern Portfolio Theory.

This change was made in 1972, with the widespread enactment of the Uniform Management of Institutional Funds Act. Since 1972, pensions have been full-on participants in the Wall Street panopticon for speculating on valuations in the valuations markets, buying and selling stocks in pursuit of capital appreciation that can only be realized by active trading.

New Innovations in Retirement Savings

Pensions are defined benefit ("DB") plans. Actuarial risk pools, actually, that rely on the Law of Large Numbers to socialize the costs of living in retirement across a statistically significant population of current and future retirees. The inverse of life insurance. Contributions vary as actuarial calculations say are necessary to provide income security in retirement to plan participants.

Pensions have always been popular with workers, and society more generally, but problematic for plan sponsors and administrators. Since the total amount of benefits to be paid are not ever really knowable (the plans being open-ended, ongoing, regenerative and therefor evergreen), it can never be certain that contributions will be adequate. This uncertainty gets magnified many times if actuarial assumptions about investment earnings are not realized in the event.

In 1978, an alternative approach to retirement savings was written into the US tax laws, in the form of various tax-deferred savings accounts. These are known as defined contribution ("DC") plans. The amounts contributed determine the amounts available to provide income during retirement. That, together with investment gains (or losses). DC plans put the risk and responsibility for investment management on each individual saver. Income security in retirement is not really assured, as the income runs out when the savings runs out, not when retirement ends.

These DC accounts are allowed to invest savings as the saver may decide. This innovation transformed the previously sleepy mutual fund business into a major market participant.

Changing the Dynamics of the Wall Street Panopticon

The growth in professionally managed retirement plans, both DB and DC, since the 1970s has been explosive. Not just in the US. Worldwide. According to research by Towers, Watson, globally, professionally managed DB and DC plans, combined, doubled over the 10 years from 2002 to 2012, from $15 Trillion to $30 Trillion USD. This represents something like half of the total estimated $60 Trillion USD available as capital for investment, worldwide.

This explosive growth in professionally managed retirement plans has transformed the dynamics of the Wall Street Panopticon. There is room for debate over whether that transformation is for the better.

Redistributing Control Over Savings Held for Investment

The diagram below shows the current state of the Wall Street Panopticon, with most of the money available for trading controlled by Mutual Funds and Pension Funds, and with a proliferation of advisors attaching themselves to the lines that connect Pension Funds especially, but Mutual Funds as well, out on the periphery with the Wall Street market-clearing mechanisms at the hub.

Creative Capitalism Becomes Casino Capitalism

Whatever one may think of the larger impact of this redistribution of control over savings held for investment, its impact on pension funds, in particular, has been adverse. Pensions are experiencing erratic returns, inadequate returns, misalignment of incentives, miscreant market manipulation, the orphaning of social, economic and environmental impacts and a growth in the zero-sum game of extracting value from other market participants, which means increasingly that each retirement plan is seeking to provide for its retirees at the expense of other retirement plans, and other retirees, who are participating in those other plans.

The "everybody wins" of wealth creating capitalism in its original incarnation has degenerated into the zero-sum game of Casino Capitalism that we are living with today. In consequence, there are those who contend that proper pension plans, DB plans that provide real, sustainable income security in retirement, cannot continue.

As the global financial crisis of 2008 demonstrated most recently and most dramatically, we all suffer adversely from this, as closed-loop trading of retirement savings drives overvaluations in the valuations markets that are unsustainable, creating an illusory prosperity that evaporates when the valuations collapse. We are getting too-big-to-fail that fails nonetheless.

A Copernican Solution: the Evergreen Stewardship Panopticon

The solution is not to be found by tweaking the current Wall Street Panopticon.

The solution is Copernican. We have to build a new stewardship panopticon that puts professional management of retirement savings at the center of its own investment universe, building for these stewards of open-ended, ongoing, regenerative - and therefor evergreen - trusts clear sight lines into equally open-ended, ongoing, regenerative and therefor evergreen wealth creation through direct engagement with wealth creating enterprises that are also open-ended, ongoing, regenerative, and therefor evergreen.

This is a natural match of evergreen to evergreen through direct participation in wealth creation over time that will empower pensions, in particular, to engineer portfolio returns to match their fiduciary responsibilities and reduce their exposure to systemic overvaluations in the valuations markets, while also simplifying portfolio design, internalizing portfolio management (to the extent they choose), reducing portfolio costs and increasing their control over portfolio impacts on society, the economy and the environment. It will empower defined benefit plans to continue providing real income security in retirement to successive generations of current and future retirees.

In this new evergreen stewardship panopticon, Wall Street is moved from the center to the periphery, where it continues to compete, as one enterprise among others, for funding from the stewards of our retirement security.

This is what makes it Copernican. The earth is no longer the center of the heavens, in which the sun is one object among many. Instead, we have a solar system, with the sun at the center, and the earth, as one planet among many, orbiting around the sun.

The post-Copernican Wall Street Panopticon

In this post-Copernican world, Wall Street will continue as the hub of its own panopticon for speculating on valuations in the valuations markets, with retirement stewards still forming one of many classes of market participants out on the periphery, but the volume of retirement savings being used to fund speculation on valuations within the New Wall Street Panopticon will shrink.

Regenerating Creative Capitalism

In the process, we will see Casino Capitalism shrink back down to a more authentic form of Creative Capitalism, but the new Creative Capitalism will be turbo-charged by access to two competing market systems: the familiar Wall Street panopticon for speculating on valuations in the valuations markets, and the new Stewardship Panopticon for direct engagement of evergreen trusts with evergreen enterprise for evergreen sharing in evergreen wealth creation.

Spatial Representation of the Copernican Revolution in Panopticons for Creative Capitalism

The Current Wall Street Panopticon

Saturday, September 14, 2013

The Solution Requires a New Panopticon.

The problem is obvious from the diagram below. A proliferation of advisers are attaching themselves to the line connecting pensions to the hub of the Wall Street panopticon, speculating on valuations in the valuations markets.

The solution is not obvious. It cannot bee seen in the diagram below.

It requires a new panopticon.

The solution is not obvious. It cannot bee seen in the diagram below.

It requires a new panopticon.

Friday, September 13, 2013

We Have to Put an End to Casino Capitalism

We have to put an end to Casino Capitalism.

We can do that by building a new investing ecosystem of evergreen cash flow sharing between evergreen trusts and evergreen enterprise, for an evergreen prosperity.

By evergreen, I mean ongoing. An evergreen investment is an agreement for the sharing out of cash flows between enterprise leaders and their capital sponsors that is open-ended and ongoing. An evergreen trust is a pension, endowment, foundation or other steward of other people's money entrusted to their care for ongoing investment and reinvestment to support the payment of chartered benefits to successive generations of charter beneficiaries that are ongoing and evergreen. An evergreen enterprise is any enterprise organized to generate cash flows through commercial competitiveness that is ongoing, and evergreen.

Evergreen prosperity just keeps going.

The paradigm shift to evergreen investing will be a Copernican Revolution in pension investing, putting pensions and other evergreen trusts at the center of their own investing universe of direct connections with enterprise leaders.

This is important because Casino Capitalism is killing defined benefit pension plans, and threatening retirement income security, in general.

Defined benefit pension plans are suffering a chronic condition of underfunding that is driving them to increase their risk on investment in pursuit of higher returns. This is only increasing their exposure to systemic risk, further undermining their ability to continue, and to continue providing income security in retirement to successive generations of current and future retirees.

We all suffer when pensions suffer the erratic returns, inadequate returns, misalignment of incentives, miscreant market manipulation, and the orphaning of social and environmental impacts through Casino Capitalism and the zero-sum games of extracting value from other investors that too often is what pension investing has really become today.

In a new evergreen investing ecosystem, pensions will be able to engineer returns to match their fiduciary responsibilities, putting them on a path to reversing the problem of underfunding and reducing their exposure to systemic risk while also simplifying their portfolio designs, internalizing portfolio management, reducing portfolio costs and controlling portfolio impacts.

In this new evergreen investing ecosystem enterprise leaders will also freed from the inauthenticity of quarterly financial reporting so they can focus more authentically on optimizing the commercial competitiveness of the enterprises they lead.

Evergreen investing will return Capitalism to its roots.

How do we act?

We need to come together as a community and have a conversation about this idea of evergreen investing. We need to imagine how it will work and how will improve outcomes. We need to clear a space where we can give it a try, work through the granularities of its implementation and see if it takes hold along the edges before swooshing into the mainstream, following the well-trodden path of other similarly disruptive, but needed and important, innovations.

Won't you join the conversation? Won't you help put an end to Casino Capitalism?

We can do that by building a new investing ecosystem of evergreen cash flow sharing between evergreen trusts and evergreen enterprise, for an evergreen prosperity.

By evergreen, I mean ongoing. An evergreen investment is an agreement for the sharing out of cash flows between enterprise leaders and their capital sponsors that is open-ended and ongoing. An evergreen trust is a pension, endowment, foundation or other steward of other people's money entrusted to their care for ongoing investment and reinvestment to support the payment of chartered benefits to successive generations of charter beneficiaries that are ongoing and evergreen. An evergreen enterprise is any enterprise organized to generate cash flows through commercial competitiveness that is ongoing, and evergreen.

Evergreen prosperity just keeps going.

The paradigm shift to evergreen investing will be a Copernican Revolution in pension investing, putting pensions and other evergreen trusts at the center of their own investing universe of direct connections with enterprise leaders.

This is important because Casino Capitalism is killing defined benefit pension plans, and threatening retirement income security, in general.

Defined benefit pension plans are suffering a chronic condition of underfunding that is driving them to increase their risk on investment in pursuit of higher returns. This is only increasing their exposure to systemic risk, further undermining their ability to continue, and to continue providing income security in retirement to successive generations of current and future retirees.

We all suffer when pensions suffer the erratic returns, inadequate returns, misalignment of incentives, miscreant market manipulation, and the orphaning of social and environmental impacts through Casino Capitalism and the zero-sum games of extracting value from other investors that too often is what pension investing has really become today.

In a new evergreen investing ecosystem, pensions will be able to engineer returns to match their fiduciary responsibilities, putting them on a path to reversing the problem of underfunding and reducing their exposure to systemic risk while also simplifying their portfolio designs, internalizing portfolio management, reducing portfolio costs and controlling portfolio impacts.

In this new evergreen investing ecosystem enterprise leaders will also freed from the inauthenticity of quarterly financial reporting so they can focus more authentically on optimizing the commercial competitiveness of the enterprises they lead.

Evergreen investing will return Capitalism to its roots.

How do we act?

We need to come together as a community and have a conversation about this idea of evergreen investing. We need to imagine how it will work and how will improve outcomes. We need to clear a space where we can give it a try, work through the granularities of its implementation and see if it takes hold along the edges before swooshing into the mainstream, following the well-trodden path of other similarly disruptive, but needed and important, innovations.

Won't you join the conversation? Won't you help put an end to Casino Capitalism?

Thursday, September 12, 2013

The Foreign Language of Speculation on Valuation over an Exchange

In an side bar email exchange with a fellow discussant from Paul Barnett's Strategic Management Bureau discussion group, I focused on cash flow as the natural language of enterprise leadership.

A moment's reflection will show that cash flow is, or should also be, the natural language of pensions and other stewards of evergreen trusts. A pension, after all, is really an enterprise in its own right. A not-for-profit enterprise, to be sure, but still an enterprise. Its business is to generate cash flows from a combination of plan contributions and investment earnings to support benefit payouts and its own operating expenses. This is all about cash flow. We call the pension trust evergreen because it is chartered to keep this ongoing.

In an evergreen investing scenario, the direct connection between enterprise leaders and stewardship investors will be eased and facilitated by the fact that the investment is constructed in the native tongues of both enterprise and investment, the language of cash flow.

Compare this to the current situation, where enterprise is funded through the Exchange, and investment is directed into enterprise indirectly, through the Exchange (or some private alternative valuation mechanism).

In this Exchange-funded paradigm, even though both enterprise and investment speak the same language, naturally, each is artificially compelled to communicate to the other only indirectly, and in the foreign language of speculation on valuations, using the Exchange as their connector and interpreter.

Another reason why, after getting over the initial culture shock of exiting their current network of peers and colleagues who all speak the language of valuations, pensions and other stewards of evergreen trusts that adopt an evergreen investment paradigm will soon settle into a comfortable routine of speaking with sponsored enterprises in their own, shared native tongue of cash flow.

A moment's reflection will show that cash flow is, or should also be, the natural language of pensions and other stewards of evergreen trusts. A pension, after all, is really an enterprise in its own right. A not-for-profit enterprise, to be sure, but still an enterprise. Its business is to generate cash flows from a combination of plan contributions and investment earnings to support benefit payouts and its own operating expenses. This is all about cash flow. We call the pension trust evergreen because it is chartered to keep this ongoing.

In an evergreen investing scenario, the direct connection between enterprise leaders and stewardship investors will be eased and facilitated by the fact that the investment is constructed in the native tongues of both enterprise and investment, the language of cash flow.

Compare this to the current situation, where enterprise is funded through the Exchange, and investment is directed into enterprise indirectly, through the Exchange (or some private alternative valuation mechanism).

In this Exchange-funded paradigm, even though both enterprise and investment speak the same language, naturally, each is artificially compelled to communicate to the other only indirectly, and in the foreign language of speculation on valuations, using the Exchange as their connector and interpreter.

Another reason why, after getting over the initial culture shock of exiting their current network of peers and colleagues who all speak the language of valuations, pensions and other stewards of evergreen trusts that adopt an evergreen investment paradigm will soon settle into a comfortable routine of speaking with sponsored enterprises in their own, shared native tongue of cash flow.

Subscribe to:

Posts (Atom)